# Import necessary libraries

import numpy as np

import pandas as pd

import statsmodels.formula.api as smf

import statsmodels.api as sm

import seaborn as sns

import matplotlib.pyplot as plt

from statsmodels.stats.outliers_influence import variance_inflation_factor5 Beyond Fit (implementation)

# Load the Boston Housing dataset (for demonstration purposes)

df = pd.read_csv('datasets/Housing.csv')

df.head()| price | area | bedrooms | bathrooms | stories | mainroad | guestroom | basement | hotwaterheating | airconditioning | parking | prefarea | furnishingstatus | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 13300000 | 7420 | 4 | 2 | 3 | yes | no | no | no | yes | 2 | yes | furnished |

| 1 | 12250000 | 8960 | 4 | 4 | 4 | yes | no | no | no | yes | 3 | no | furnished |

| 2 | 12250000 | 9960 | 3 | 2 | 2 | yes | no | yes | no | no | 2 | yes | semi-furnished |

| 3 | 12215000 | 7500 | 4 | 2 | 2 | yes | no | yes | no | yes | 3 | yes | furnished |

| 4 | 11410000 | 7420 | 4 | 1 | 2 | yes | yes | yes | no | yes | 2 | no | furnished |

# build a formular api model using price as the target, the rest of the variables as predictors

model = smf.ols('price ~ area + bedrooms + bathrooms + stories + mainroad + guestroom + basement + hotwaterheating + airconditioning + parking + prefarea + furnishingstatus', data=df)

model = model.fit()

print(model.summary()) OLS Regression Results

==============================================================================

Dep. Variable: price R-squared: 0.682

Model: OLS Adj. R-squared: 0.674

Method: Least Squares F-statistic: 87.52

Date: Wed, 05 Feb 2025 Prob (F-statistic): 9.07e-123

Time: 08:46:02 Log-Likelihood: -8331.5

No. Observations: 545 AIC: 1.669e+04

Df Residuals: 531 BIC: 1.675e+04

Df Model: 13

Covariance Type: nonrobust

======================================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------------------

Intercept 4.277e+04 2.64e+05 0.162 0.872 -4.76e+05 5.62e+05

mainroad[T.yes] 4.213e+05 1.42e+05 2.962 0.003 1.42e+05 7.01e+05

guestroom[T.yes] 3.005e+05 1.32e+05 2.282 0.023 4.18e+04 5.59e+05

basement[T.yes] 3.501e+05 1.1e+05 3.175 0.002 1.33e+05 5.67e+05

hotwaterheating[T.yes] 8.554e+05 2.23e+05 3.833 0.000 4.17e+05 1.29e+06

airconditioning[T.yes] 8.65e+05 1.08e+05 7.983 0.000 6.52e+05 1.08e+06

prefarea[T.yes] 6.515e+05 1.16e+05 5.632 0.000 4.24e+05 8.79e+05

furnishingstatus[T.semi-furnished] -4.634e+04 1.17e+05 -0.398 0.691 -2.75e+05 1.83e+05

furnishingstatus[T.unfurnished] -4.112e+05 1.26e+05 -3.258 0.001 -6.59e+05 -1.63e+05

area 244.1394 24.289 10.052 0.000 196.425 291.853

bedrooms 1.148e+05 7.26e+04 1.581 0.114 -2.78e+04 2.57e+05

bathrooms 9.877e+05 1.03e+05 9.555 0.000 7.85e+05 1.19e+06

stories 4.508e+05 6.42e+04 7.026 0.000 3.25e+05 5.77e+05

parking 2.771e+05 5.85e+04 4.735 0.000 1.62e+05 3.92e+05

==============================================================================

Omnibus: 97.909 Durbin-Watson: 1.209

Prob(Omnibus): 0.000 Jarque-Bera (JB): 258.281

Skew: 0.895 Prob(JB): 8.22e-57

Kurtosis: 5.859 Cond. No. 3.49e+04

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 3.49e+04. This might indicate that there are

strong multicollinearity or other numerical problems.# ------------------------------------------

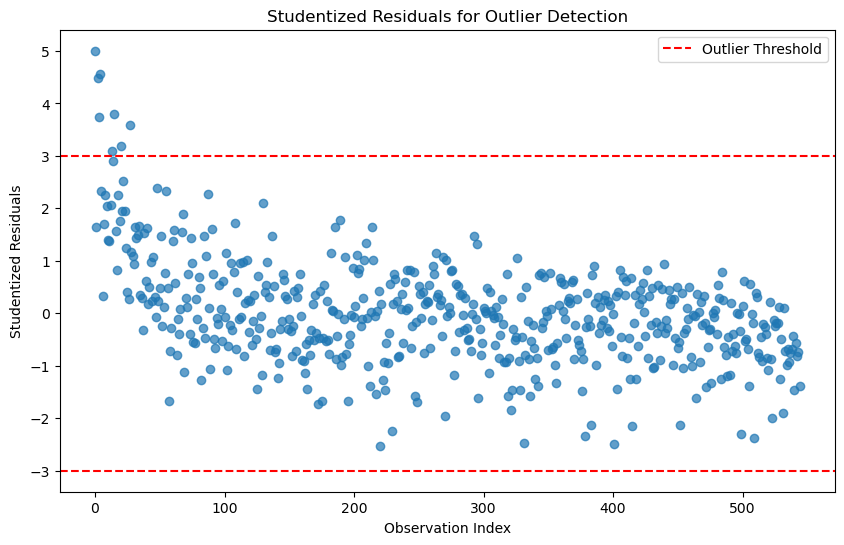

# 1. Identifying Outliers (using studentized residuals)

# ------------------------------------------

# Outliers can be detected using studentized residuals

outliers_studentized = model.get_influence().resid_studentized_external

outlier_threshold = 3 # Common threshold for studentized residuals# Plot studentized residuals

plt.figure(figsize=(10, 6))

plt.scatter(range(len(outliers_studentized)), outliers_studentized, alpha=0.7)

plt.axhline(y=outlier_threshold, color='r', linestyle='--', label='Outlier Threshold')

plt.axhline(y=-outlier_threshold, color='r', linestyle='--')

plt.title('Studentized Residuals for Outlier Detection')

plt.xlabel('Observation Index')

plt.ylabel('Studentized Residuals')

plt.legend()

plt.show()

# Identify observations with high studentized residuals

outlier_indices_studentized = np.where(np.abs(outliers_studentized) > outlier_threshold)[0]

print(f"Outliers detected at indices: {outlier_indices_studentized}")Outliers detected at indices: [ 0 2 3 4 13 15 20 27]# ------------------------------------------

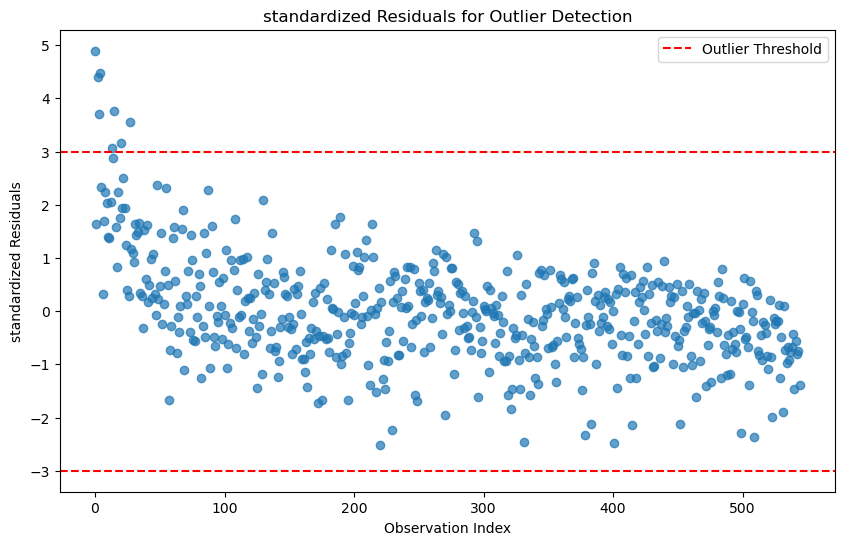

# 1. Identifying Outliers (using standardized residuals)

# ------------------------------------------

# Outliers can be detected using standardized residuals

outliers_standardized = model.get_influence().resid_studentized_internal

outlier_threshold = 3 # Common threshold for standardized residuals# Identify observations with high standardized residuals

outlier_indices_standardized = np.where(np.abs(outliers_standardized) > outlier_threshold)[0]

print(f"Outliers detected at indices: {outlier_indices_standardized}")Outliers detected at indices: [ 0 2 3 4 13 15 20 27]# Plot studentized residuals

plt.figure(figsize=(10, 6))

plt.scatter(range(len(outliers_standardized)), outliers_standardized, alpha=0.7)

plt.axhline(y=outlier_threshold, color='r', linestyle='--', label='Outlier Threshold')

plt.axhline(y=-outlier_threshold, color='r', linestyle='--')

plt.title('standardized Residuals for Outlier Detection')

plt.xlabel('Observation Index')

plt.ylabel('standardized Residuals')

plt.legend()

plt.show()

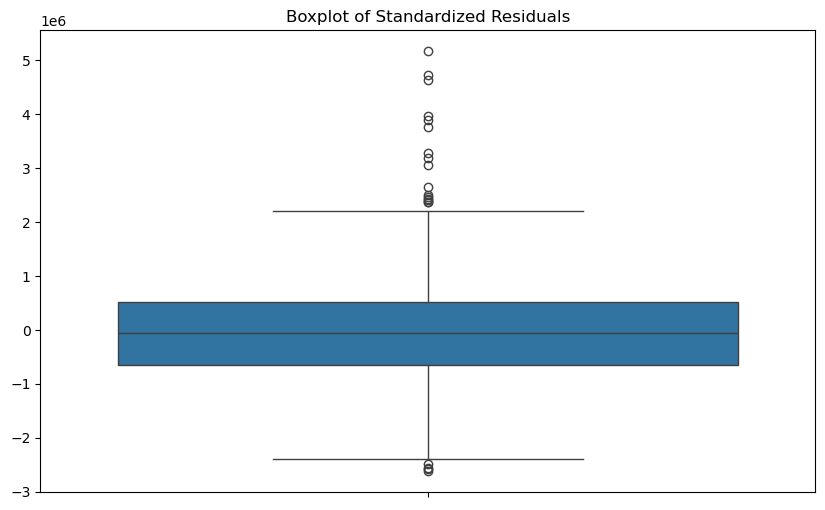

# ------------------------------------------

# 1. Identifying Outliers (using boxplot)

# ------------------------------------------

# Outliers can be detected using boxplot of standardized residuals

plt.figure(figsize=(10, 6))

sns.boxplot(model.resid)

plt.title('Boxplot of Standardized Residuals');

# use 3 standard deviation rule to identify outliers

outlier_indices = np.where(np.abs(model.resid) > 3 * model.resid.std())[0]

print(f"Outliers detected at indices: {outlier_indices}")Outliers detected at indices: [ 0 2 3 4 13 15 20 27]# ------------------------------------------

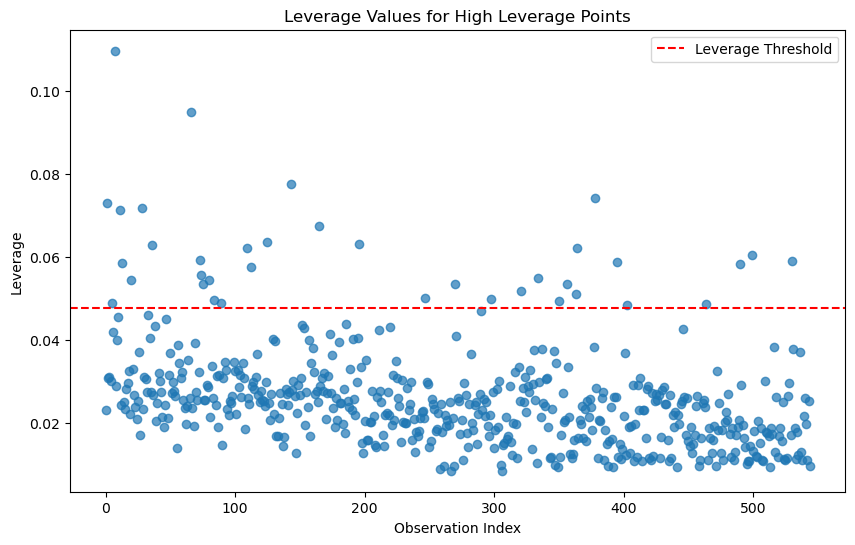

# 2. Identifying High Leverage Points

# ------------------------------------------

# High leverage points can be detected using the hat matrix (leverage values)

leverage = model.get_influence().hat_matrix_diag

leverage_threshold = 2 * (df.shape[1] / df.shape[0]) # Common threshold for leverage5.0.0.1 Identifying High Leverage Points

A common threshold for identifying high leverage points in regression analysis is:

\(h_i > \frac{2p}{n}\)

where:

- \(h_i\) is the leverage value for the ( i )-th observation,

- \(p\) is the number of predictors (including the intercept), and

- \(n\) is the total number of observations.

# Plot leverage values

plt.figure(figsize=(10, 6))

plt.scatter(range(len(leverage)), leverage, alpha=0.7)

plt.axhline(y=leverage_threshold, color='r', linestyle='--', label='Leverage Threshold')

plt.title('Leverage Values for High Leverage Points')

plt.xlabel('Observation Index')

plt.ylabel('Leverage')

plt.legend()

plt.show()

# Identify observations with high leverage

high_leverage_indices = np.where(leverage > leverage_threshold)[0]

print(f"High leverage points detected at indices: {high_leverage_indices}")High leverage points detected at indices: [ 1 5 7 11 13 20 28 36 66 73 74 75 80 84 89 109 112 125

143 165 196 247 270 298 321 334 350 356 363 364 378 395 403 464 490 499

530]# ------------------------------------------

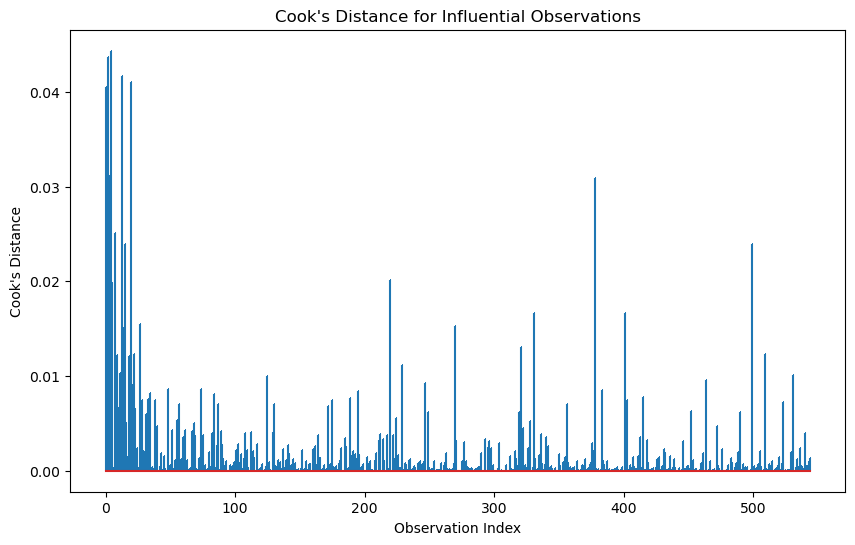

# 3. Cook's Distance for Influential Observations

# ------------------------------------------

# Cook's distance measures the influence of each observation on the model

cooks_distance = model.get_influence().cooks_distance[0]

# Plot Cook's distance

plt.figure(figsize=(10, 6))

plt.stem(range(len(cooks_distance)), cooks_distance, markerfmt=",")

plt.title("Cook's Distance for Influential Observations")

plt.xlabel('Observation Index')

plt.ylabel("Cook's Distance")

plt.show()

Cook’s distance is considered high if it is greater than 0.5 and extreme if it is greater than 1.

# Identify influential observations

influential_threshold = 4 / (df.shape[1] - 1 ) # Common threshold for Cook's distance

influential_indices = np.where(cooks_distance > influential_threshold)[0]

print(f"Influential observations detected at indices: {influential_indices}")Influential observations detected at indices: []# =======================================

# 4. Checking Multicollinearity (VIF)

# =======================================

# VIF calculation

from statsmodels.stats.outliers_influence import variance_inflation_factor

def calculate_vif(X):

vif_data = pd.DataFrame()

vif_data["Variable"] = X.columns

vif_data["VIF"] = [variance_inflation_factor(X.values, i) for i in range(X.shape[1])]

return vif_data

X = df[['area', 'bedrooms', 'bathrooms', 'stories', 'mainroad', 'guestroom', 'basement', 'hotwaterheating', 'airconditioning', 'parking', 'prefarea', 'furnishingstatus']]

# one-hot encoding for categorical variables

X = pd.get_dummies(X, drop_first=True, dtype=float)

vif_data = calculate_vif(X)

print("\nVariance Inflation Factors:")

print(vif_data.sort_values('VIF', ascending=False))

Variance Inflation Factors:

Variable VIF

1 bedrooms 16.652387

2 bathrooms 9.417643

0 area 8.276447

3 stories 7.880730

5 mainroad_yes 6.884806

11 furnishingstatus_semi-furnished 2.386831

7 basement_yes 2.019858

12 furnishingstatus_unfurnished 2.008632

4 parking 1.986400

9 airconditioning_yes 1.767753

10 prefarea_yes 1.494211

6 guestroom_yes 1.473234

8 hotwaterheating_yes 1.091568# Rule of thumb: VIF > 10 indicates significant multicollinearity

multicollinear_features = vif_data[vif_data['VIF'] > 10]['Variable']

print(f"Features with significant multicollinearity: {multicollinear_features.tolist()}")Features with significant multicollinearity: ['bedrooms']# =======================================

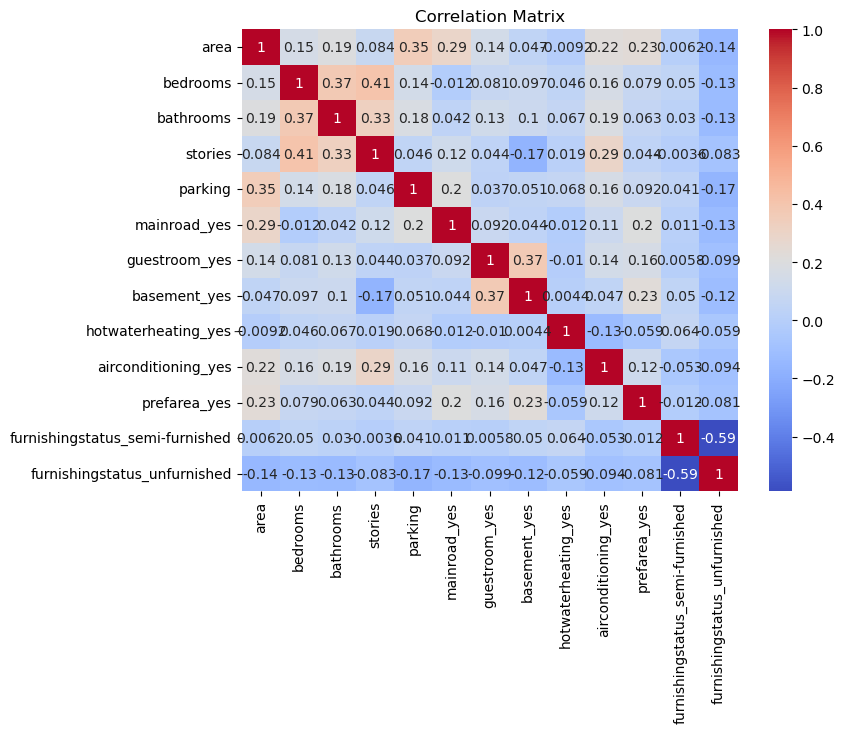

# 4. Checking Multicollinearity (Correlation Matrix)

# =======================================

# Correlation matrix

correlation_matrix = X.corr()

plt.figure(figsize=(8, 6))

sns.heatmap(correlation_matrix, annot=True, cmap='coolwarm')

plt.title('Correlation Matrix');

#output the correlation of other predictors with the bedrooms

X.corr()['bedrooms'].abs().sort_values(ascending=False)bedrooms 1.000000

stories 0.408564

bathrooms 0.373930

airconditioning_yes 0.160603

area 0.151858

parking 0.139270

furnishingstatus_unfurnished 0.126252

basement_yes 0.097312

guestroom_yes 0.080549

prefarea_yes 0.079023

furnishingstatus_semi-furnished 0.050040

hotwaterheating_yes 0.046049

mainroad_yes 0.012033

Name: bedrooms, dtype: float64# ------------------------------------------

# 5. Analyzing Residual Patterns

# ------------------------------------------

# Residuals vs Fitted Values Plot

fitted_values = model.fittedvalues

residuals = model.resid

plt.figure(figsize=(10, 6))

sns.residplot(x=fitted_values, y=residuals, lowess=True, line_kws={'color': 'red', 'lw': 1})

plt.title('Residuals vs Fitted Values')

plt.xlabel('Fitted Values')

plt.ylabel('Residuals');

# QQ Plot for Normality of Residuals

plt.figure(figsize=(10, 6))

sm.qqplot(residuals, line='s')

plt.title('QQ Plot of Residuals');

<Figure size 1000x600 with 0 Axes>

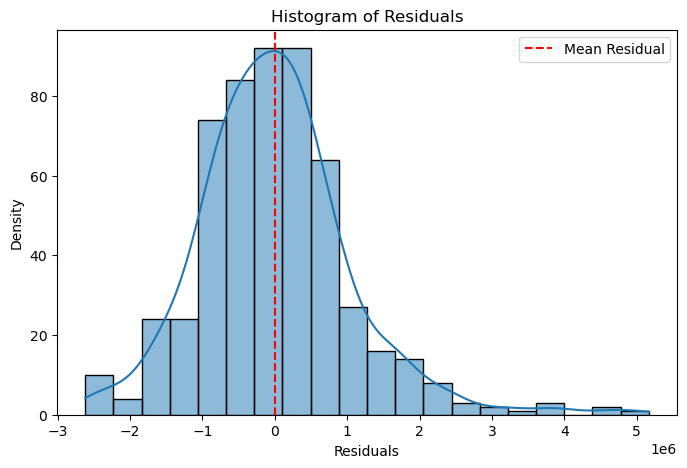

plt.figure(figsize=(8, 5))

sns.histplot(residuals, kde=True, bins=20)

plt.axvline(residuals.mean(), color='red', linestyle='--', label="Mean Residual")

plt.xlabel("Residuals")

plt.ylabel("Density")

plt.title("Histogram of Residuals")

plt.legend()

plt.show()